Thanks, that is quite different to what I thought you initially said.

I am not sure you can categorically say the NDX DAC is better than the nd5xs2 DAC however you can of course absolutely say you prefer the sound of your setup as you describe.

Thanks, that is quite different to what I thought you initially said.

I am not sure you can categorically say the NDX DAC is better than the nd5xs2 DAC however you can of course absolutely say you prefer the sound of your setup as you describe.

A 33% YoY drop in revenue is pretty severe. No amount of cost cutting is going to offset that. New products and services to the rescue please.

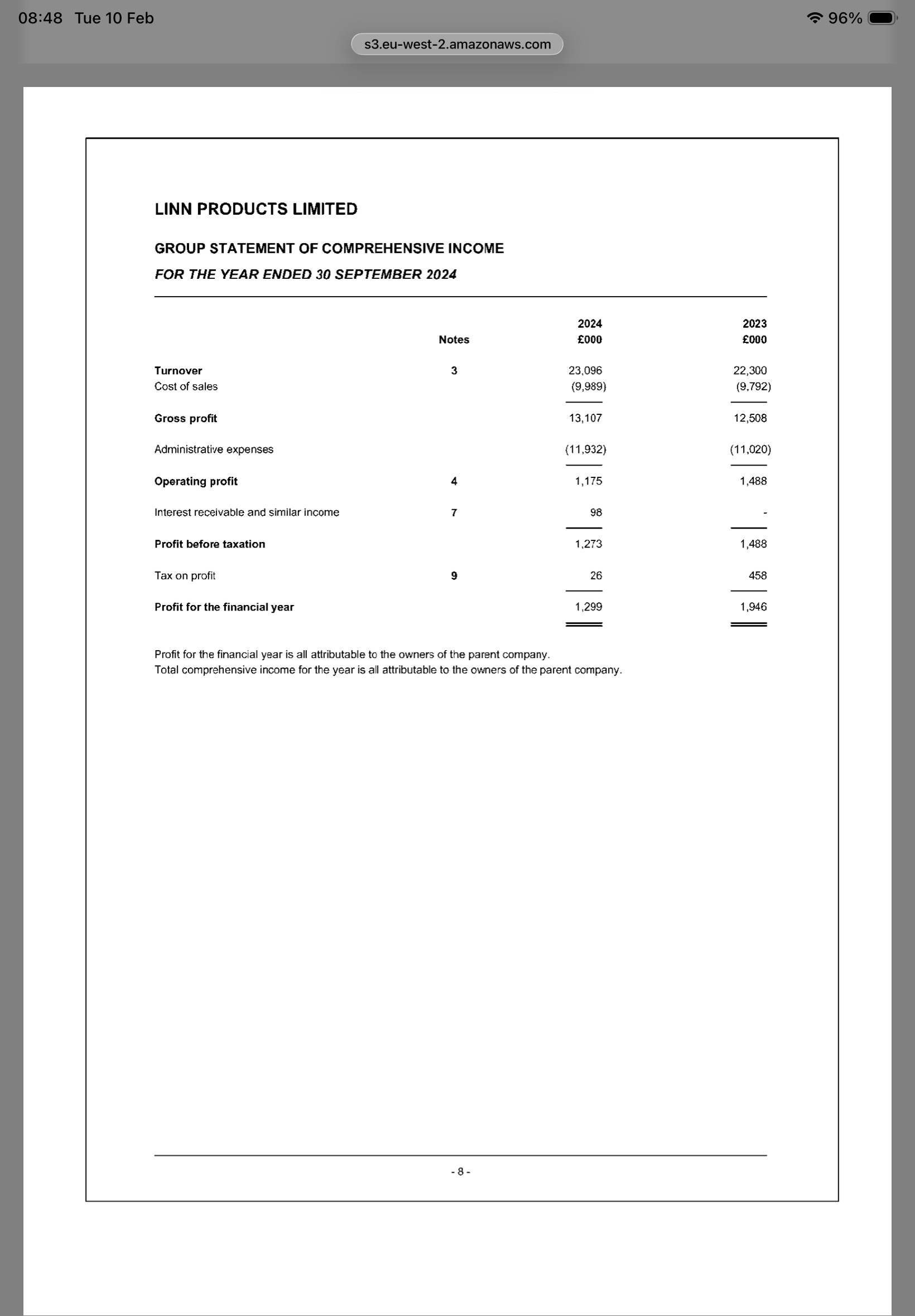

Would be interesting to see another company profile to see the trend comparison.

Linn would be notable comparison.

Hmmmm, not a very reassuring comparison unfortunately.

Whilst I agree that the category includes the overheads, etc., it is not certain that there are no group charges in there as they have taken advantage of the exemption from disclosing related party transactions between group members.

Revenue up YoY. It’s only SG&A costs dragging the bottom line down.

that’s why I love this forum, cheers @Gazza.

I cannot remember the timeline of when Naim had to discontinue each product. But as they were forced to withdraw perhaps those loss of sales partly or fully explains some of the losses?

I mentioned Linn as an example deliberately (without knowing what the answers were) as they present some interesting similarities and indeed differences.

Some of the below are generalisations but probably accepted by most as true.

The 33% drop in revenue is catastrophic, can you imagine anyone at the start of that financial year presenting such a case and getting signoff on it as part of a business plan, just wouldn’t happen. That’s the sort of results that get people fired and not always the right ones.

Then take the products that can no longer be produced due to inability to source components, there are various reasons behind why they may not be able to be sourced but there has been a trend that they haven’t been able to plan for.

Now look at their traditional business model, we are a massively loyal customer base and most of us started with one product lower in the range and followed the revenue structure of incremental power supplies then up in the food chain etc. This also meant a really healthy (some of the best) market on pre-loved, which brought more into the fold. As many have posted the used market is apparently on its knees too.

Well the food chain isn’t there anymore, indeed the Nait 50 showed a product that failed on launch at its price, got massively discounted and then against the established food chain went and cannibalised the big systems (admittedly its a small example segment).

Maybe Linn’s reduced product range is the way Naim is headed, I mean its not like they have had an Intek / CD Player or anything for an age.

Definitely concerning and the revenue drop would not have been planned for at those levels.

There are compound issues at play here, market is changing very rapidly, and the established market is shrinking.

Really hope Naim can come out swinging from all of this, brilliant products that have brought joy and continue to, here’s hoping that continues for decades to come.

One thing I remember from my most recent factory visit (Dan’s trip) was a comment that roughly the revenue split for Naim then was Muso around 40%, Uniti 30+% and the separates around 30%. At the end of 2024 Naim discontinued the Qb2, which I suspect was the larger selling unit of the range. That. in itself would lead to a revenue drop of 20+%. It really surprises me that Naim discontinued what seems to have been a really successful product without a replacement or any way to fill that revenue gap, given that it seems to fit into the market segments they are (as far as I can see) looking to address.

Of note, direct costs only decreased 30% so there’s some significant margin leakage there. Again, need more affordable products with decent margins or super high end products with eye-watering margins.

Out of interest, does anyone have the 21 and 22 accounts to hand? A one year comparison could include any number of one offs and the like. And if this is derailing the thread, maybe we move it to its own discussion. The coprorate guys would love that…![]()

Regarding the QB2, I remember a while back visiting the dealer ‘HiFi Lounge’ to collect something. I was waiting near their front desk and remember mentioning ‘that sounds nice, what’s playing?’

She pointed to the QB2, that!

I thought wow, that’s a lovely sound. No wonder it was a great seller considering its price point and performance.

Linn achieves a gross margin of 56% vs Naim’s 35% suggesting Naim’s production costs are much higher (higher Cost of Sales relative to Turnover). This could be partly down to location, i.e. higher salaries of production employees in Salisbury vs Aberdeen, but more likely due to an inefficient and expensive supply chain and manufacturing process, including potentially more expensive components/materials.

I think comparing profits/loss would be more interesting against Rega figures

Glasgow. No Linn here in the Tundra.

Go for it

They are all on the Companies House website. 2021 saw a huge rise in turnover and that peaked in 2022 at £41.3m, a modest drop in 2023 and fell off its perch in 2024 but I haven’t delved into the profits/losses in any detail.

Interestingly it appears* that the R&D section was given a very sizeable employee boost in 2024.

*Difficult to be certain becaue of the damn fool way that number has to be calculated under the law.

I think the Pandemic had weird effects on sales , lots of stock shifted .